The Arcadis Market View Spring 2025 warns of a bleak future for the industry in 2025 with no recovery expected until late in the year.

The post The Arcadis Market View Spring 2025 shows a rough future appeared first on Planning, Building & Construction Today.

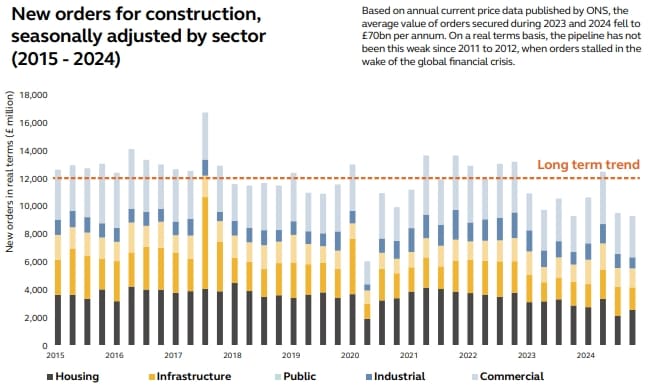

The Market View states that growth marked the end of 2024, but that the industry is not out of the woods yet

The Market View Spring 2025, subtitled Wishing and Hoping, shows that the second half of 2024 saw marginal growth, meaning that the construction sector’s contraction has come to an end.

However, issues including lack of confidence and growth, and rising costs are continuing issues holding the industry back.

No recovery before Q4 2025, says Market View Spring 2025

The report breaks down the industry by sector with predictions based on current climate, investments, and past performance:

- Resilience – Including water and energy, the resilience sector is predicted to become the most active sector in the UK’s construction industry, due to investments into energy transition and water networks, with a £20bn portfolio of Accelerated Strategic Transmission Investment, and £44bn for water network enhancements, the resilience pipeline is diverse.

- Mobility – This sector includes road, rail, ports, airports, etc. and represents both public and private investment. The report notes this sector as a mixed bag, with higher profile projects such as Lower Thames Crossing and both Luton and Gatwick airport investments contrasting with delays to the National Highways RIS3 programme, and devolution of spending to combined authorities extending periods of planning and procurement.

- Places – This sector includes public and private investment into housing and infrastructure such as schools, hospitals, and commercial offices. The report notes a jump in volume of orders for public buildings by 8% in 2024, but casts doubt on whether this will be a longer-term trend due to a history of public sector buildings have been overshadowed by large transport schemes and investment into for-sale and leasing markets.

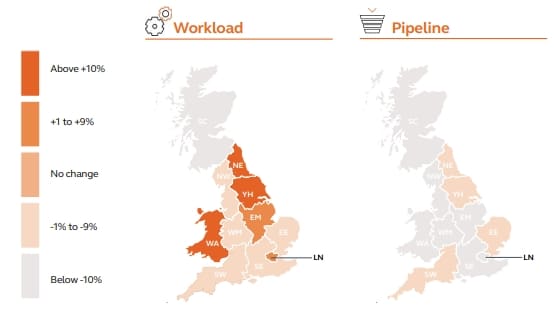

Weak future workload pipeline cause for concern

The report delves into new orders, pulling some concerning trends from the data, with no growth in orders since July 2024 and representing a nearly 20% drop. Coupled with a continually flatlining economy, the future looks troublesome for this statistic.

This falls in line with the recent S&P PMI report as well.

The report lists:

- The housing pipeline remains the weakest, with orders in 2024 the lowest since 2009, and high-density developments being stalled but viability and safety issues.

- Industrial and commercial starts slowed at the end of 2024, highlighting developer sentiment on rising long-term finance costs and less business confidence across the sector.

- Public sector non-residential new orders have also dropped since Q2 2024, in spite of the increased output.

- New workload for the rail sector has not increased but remained steady, with most workloads being for renewal rather than enhancement.

- New road projects have also remained stagnant with planning consents and delays to finalising the RIS3 project will be a part of the coming spending review.

Simon Rawlinson, Arcadis head of strategic research and insight, said: “The UK construction sector has reached a turning point, with marginal growth in late 2024 marking the end of contraction. However, the outlook remains uncertain, with a weakening future pipeline posing a serious concern.

“New orders have dropped sharply, and while infrastructure investment is set to rise, commercial and residential recovery remains sluggish due to low confidence and high finance costs. The shift towards low-rise residential schemes highlights ongoing regulatory challenges, while resource constraints in the resilience sector could drive inflationary pressures.

“Without renewed investor confidence and strategic government action, a sustained recovery is far from guaranteed.”

Stuart Humber, Arcadis UK&I service lead, resilience, said: “The resilience sector is set to be one of the most active in UK construction, driven by major investments in energy transition, water networks, and flood protection. With a £20bn portfolio of ASTI transmission projects and £44bn for water network enhancements, few sectors can match its scale and diversity.

“However, with AMP8 now moving forward, water companies are relying on an already stretched supply chain to rapidly scale up. Labour market constraints and procurement challenges for specialist equipment could drive inflationary pressures while planning reforms may add further competition for resources as the renewables sector accelerates investment.”

The report can be read in full here.

The post The Arcadis Market View Spring 2025 shows a rough future appeared first on Planning, Building & Construction Today.